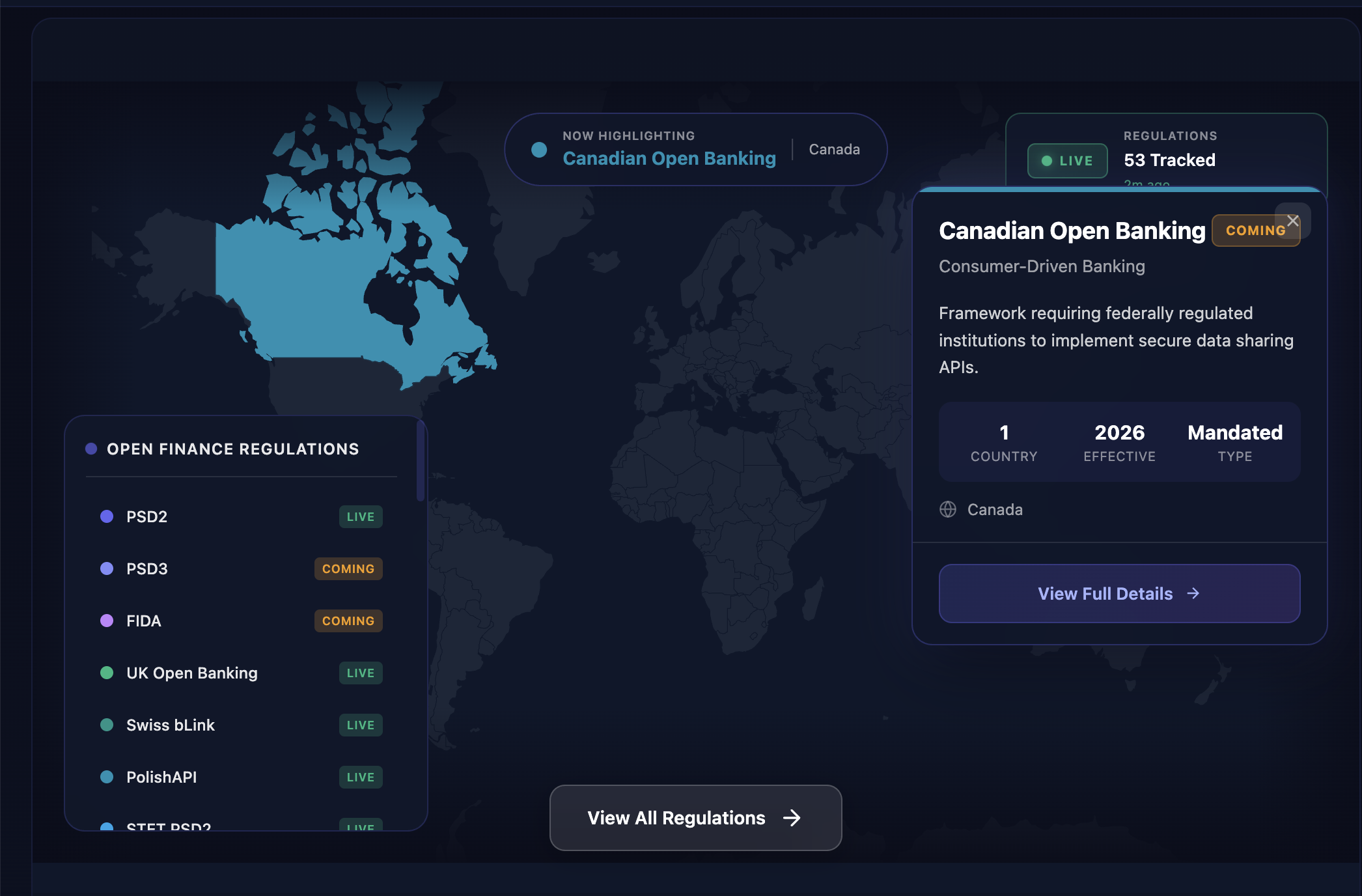

Canada has a law, a regulator, and a two-phase roadmap for open banking. What it does not yet have is a launch date.

That distinction matters. As of March 5, 2026, the Bank of Canada's head of payments, Ron Morrow, told attendees at the Open Banking Expo in Toronto that it would be "premature and ill-advised" to commit to a date until the required work is fully understood. Participants should expect "an appropriate amount of lead time" for compliance once a timeline is confirmed. A 2026 launch is widely seen as at risk.

That is the honest starting point. Here is what the framework says, what is actually settled, and where the real uncertainties sit.

A Long Time Coming

Canada's open banking journey began in earnest in 2018 with an advisory committee and a series of consultation rounds. The country originally targeted January 2023 as an "ambitious but achievable" launch date. That came and went. Parliament prorogued in January 2025, pausing progress again. Budget 2025 finally changed the picture.

The Consumer-Driven Banking Act (CDBA) received its first Royal Assent in June 2024, establishing a foundational framework but leaving the substantive details, including accreditation, liability rules, and national security safeguards, for later legislation. Bill C-15, tabled November 18, 2025, introduced those remaining pieces as part of the Budget Implementation Act. As of March 2026, Bill C-15 is still before Parliament.

What Budget 2025 Actually Confirmed

Budget 2025 locked in several things that had been contested or uncertain.

The Bank of Canada replaced the Financial Consumer Agency of Canada (FCAC) as the primary supervisory authority. The BoC already oversees the Retail Payment Activities Act and the registry of payment service providers, so the consolidation creates a cleaner governance line. The government allocated up to CAD 19.3 million to the Bank of Canada over two years for implementation, with administrative costs of approximately CAD 5 million per year thereafter.

The budget also confirmed a two-phase roadmap: Phase 1 covering read-only data sharing, and Phase 2 covering write access including payment initiation and account switching. Phase 2 is explicitly tied to the Real-Time Rail (RTR) being live and in widespread use.

The budget also introduced an amendment to the Personal Information Protection and Electronic Documents Act (PIPEDA) to establish an economy-wide data mobility right, with consumer-driven banking as its first application.

Phase 1: Read Access

Phase 1 covers read-only data sharing. Accredited providers will be able to pull transaction history, account balances, product data, and other in-scope information from participating financial institutions, with explicit consumer consent.

The scope covers deposit accounts (chequing and savings), payment products, registered and non-registered investment accounts, and lending products such as credit cards and mortgages. Derived data is excluded. If an institution has processed raw data to create a proprietary insight or score, that output sits outside the sharing mandate.

According to the Department of Finance, roughly nine million Canadians currently share their banking credentials with third-party apps through screen scraping. The Consumer-Driven Banking Act is designed to give those people a safer alternative: instead of handing over a password, consumers direct their bank to share specific data with an accredited third party over a secure API. The bank sees this as a legitimate, consumer-authorized transaction, which means existing liability protections stay intact.

Participation is mandatory for large retail banks above a threshold still to be defined in regulation. The Big Six, RBC, TD, BMO, Scotiabank, CIBC, and National Bank of Canada, will be required to participate. Credit unions and other institutions can opt in once they meet accreditation requirements.

TD Bank's vice-president for open banking, Maureen Di Sebastiano, put the consumer framing plainly at Open Banking Expo Canada in June 2025: open banking is about Canadians being empowered to use their financial data to make their lives better. The major banks are investing in implementation regardless of the exact timeline.

Phase 2: Write Access and the RTR Dependency

Phase 2 is targeted for mid-2027 and is explicitly contingent on the RTR being live and in widespread use. Write access means accredited third parties can initiate actions on behalf of consumers: making payments, switching accounts, opening new accounts, triggering lending flows.

Canada's five largest banks currently account for the majority of financial services in the country, with the Big Six holding around 93% of banking assets. Write access is where competitive dynamics could shift materially. Payment initiation alone removes interchange costs for merchants. Account switching lowers the practical barrier to changing providers. A 2024 Abacus Data poll found that two-thirds of Canadians had no intention of considering switching financial providers in the next two years. That level of inertia reflects structural friction as much as preference, and write access is the mechanism most likely to address it.

The RTR is Canada's forthcoming instant payments infrastructure, managed by Payments Canada. Budget 2025 targeted its launch in Q3 2026. Some industry observers expect it to slip to late 2026 or early 2027. Write access follows once the RTR is operational at scale, so any delay in the RTR pushes Phase 2 accordingly.

The Screen Scraping Ban

The CDBA includes a broad prohibition on screen scraping: using a consumer's authentication credentials to access their data for the purpose of providing a product or service. This ban is not yet in force. Draft regulations are expected in 2026. The prohibition takes effect only after the framework is fully operational.

For any fintech currently using credential-based data access in Canada, the transition window exists but it is finite. Building toward accredited API access is not optional, it is a matter of timing.

The Competition Bureau's Perspective

At the same March 5, 2026 event where the Bank of Canada flagged timeline uncertainty, Acting Commissioner of Competition Jeanne Pratt made a forceful case for urgency. Canada's financial sector is concentrated, barriers to entry are high, and switching frictions are real. Competition Bureau research into data portability in the insurance sector found it could save Canadians between CAD 1.1 billion and CAD 3.8 billion in annual costs, through switching to lower-priced plans and reduced time spent comparing providers.

The Bureau also found that Canadians who understand how data portability works are 37% more likely to adopt it, while those who see it as high-risk are 65% less likely to engage. That gap creates a real obligation on government and industry to communicate clearly about what the framework actually does.

The Bureau's enforcement work has already touched the space. Following a 2024 investigation into Interac's e-transfer pricing, which favored Canada's largest banks through volume-based discounts and put smaller institutions at a cost disadvantage, Interac moved to a flat-fee model in November 2025. The Bureau is continuing to monitor.

The Open Finance Gap

The CDBA covers deposit accounts and basic financial products. It does not cover mortgages as a portable data type for shopping purposes, insurance products, or the accounting and payroll data that represent a small business's most important financial record.

As Eric Saumure argued in Policy Options in December 2025, the largest financial decisions for most Canadian households are not about day-to-day transactions. They are about mortgages, insurance, and retirement savings. For a small business, the most important data live in accounting systems, payroll, and receivables, not a single bank account. A narrow version of open banking risks entrenching a two-tier system where some data are portable and some stay locked, even though they describe the same person or firm.

The PIPEDA data mobility amendment points toward a broader future, but it requires additional regulatory work to extend to those domains. The UK's open banking framework has over 12 million active users and has contributed an estimated £4 billion to the UK economy. Australia's Consumer Data Right, though slower on adoption, is now expanding into energy and telecommunications. Canada has the legislative foundation and the advantage of learning from those markets. What it needs next is a clear sequencing plan for open finance, expanding beyond banking data, and policymakers have not yet committed to one.

What Is Still Undefined

Several critical details are pending:

The Bank of Canada has not committed to a Phase 1 launch date. Regulatory timelines depend on completing the accreditation process, designating the technical standards body, and finalizing the list of mandatory participating banks.

The technical standards body has not been designated. This body will define the actual API format, authentication flows, and interoperability requirements. Without published standards, developers cannot build to a final spec.

The list of banks required to participate has not been published. The threshold for mandatory participation based on retail volume will be set in regulation.

Accreditation criteria for non-bank service providers are still being developed. Details beyond banks and registered PSPs will come in future regulatory guidance.

Liability mechanics for consumer losses are partially defined. The CDBA states consumers will not be liable for financial losses from unauthorized data access, with a carve-out for gross negligence. How consumers get made whole, and by whom, is left to regulation.

What This Means in Practice

For fintechs in Canada, Phase 1 creates the clearest near-term opportunity in use cases that work on read-only data: cash flow analysis, personal finance management, income verification, credit underwriting, and compliance tooling. These do not require the RTR.

For companies planning for 2027, write access is where embedded finance becomes commercially meaningful. Payment initiation, account funding, and account opening will all be possible through accredited APIs once the RTR is live. Organizations that engage with the accreditation process now will have an advantage when the framework goes live.

For banks, the framework is both a compliance obligation and a strategic decision point. Acting Commissioner Pratt's framing at Open Banking Expo was direct: without an open banking framework, access to data will continue to be gated by incumbents, and consumers will remain locked into relationships defined by friction rather than choice. The question for large institutions is not whether to participate but how to position as the framework matures.

Timeline Summary

- June 2024: Part 1 of the Consumer-Driven Banking Act receives Royal Assent

- November 2025: Budget 2025 confirms Bank of Canada oversight, RTR launch plan, write access target

- November 2025: Bill C-15 introduces full CDBA with accreditation and common rules (still before Parliament as of March 2026)

- November 2025: Interac moves to flat-fee e-transfer pricing model

- March 5, 2026: Open Banking Expo Canada — Bank of Canada signals no launch date committed; Competition Bureau urges urgency on competition grounds

- Q3 2026 (target): Real-Time Rail expected to launch (some estimates point to late 2026 or early 2027)

- Phase 1 (date TBC): Read access for accredited providers, once Bank of Canada completes its work and sets standards

- Mid-2027 (target): Phase 2, write access including payment initiation and account switching, contingent on RTR

Canada's open banking framework is real. The legislation is drafted, the regulator is named, and the policy intent is clear. What remains is implementation, and as of March 2026, that work is still in its early stages.

The Open Banking Tracker monitors 54,000+ financial institutions and open banking regulations across 30+ jurisdictions. For Canada-specific data see the Canada country page. For a broader view of where Canada stands globally, see the Open Finance Map.