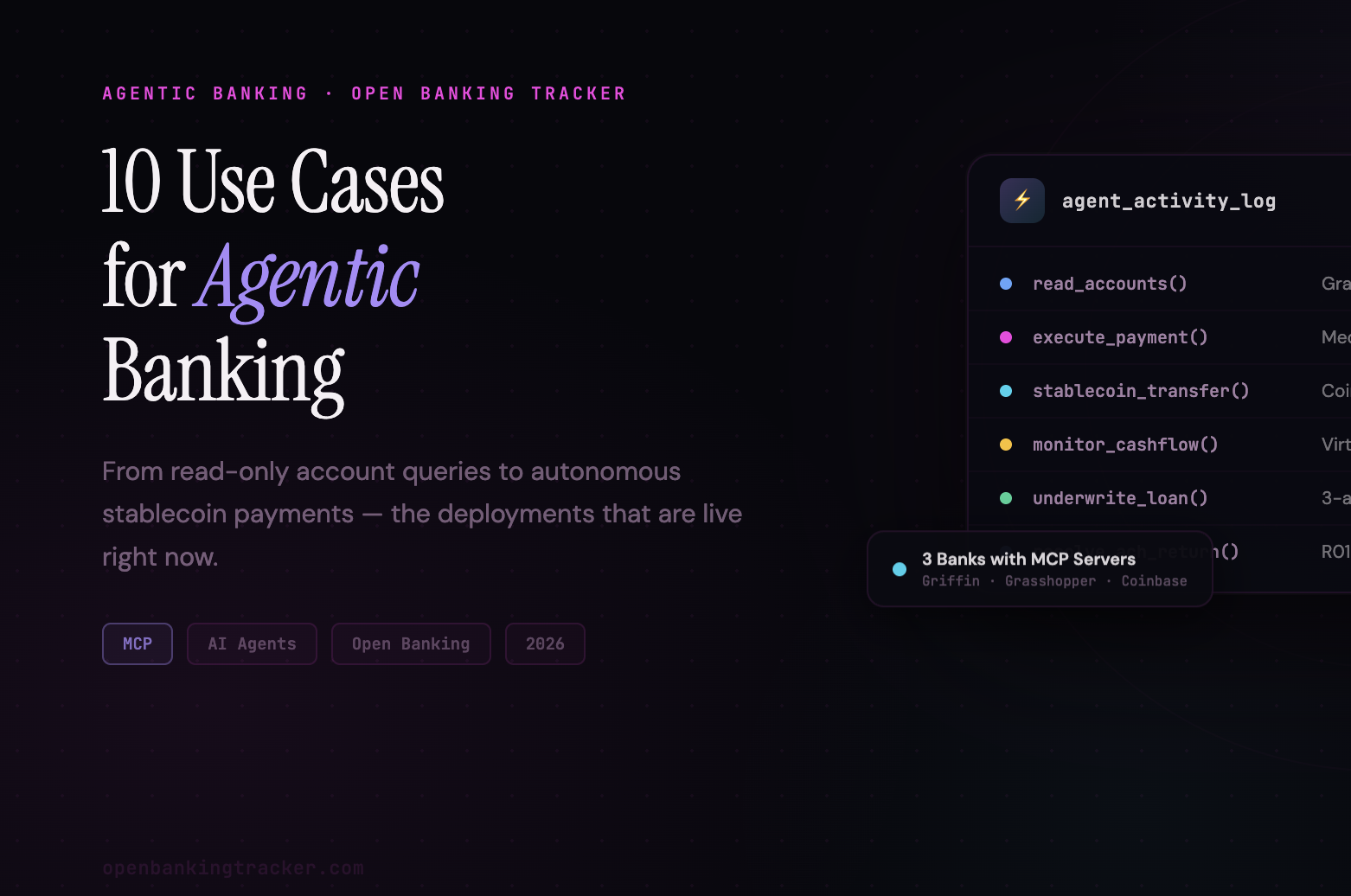

Seventy percent of banking executives say their institution is already using agentic AI in banking, according to a 2026 MIT Technology Review Insights survey of 250 banking leaders. Fraud detection, underwriting, compliance, customer service: the deployments are real. What's newer is the external layer, where AI agents connect to banking infrastructure via protocols like MCP (Model Context Protocol) to act on behalf of customers and businesses, not just internal teams.

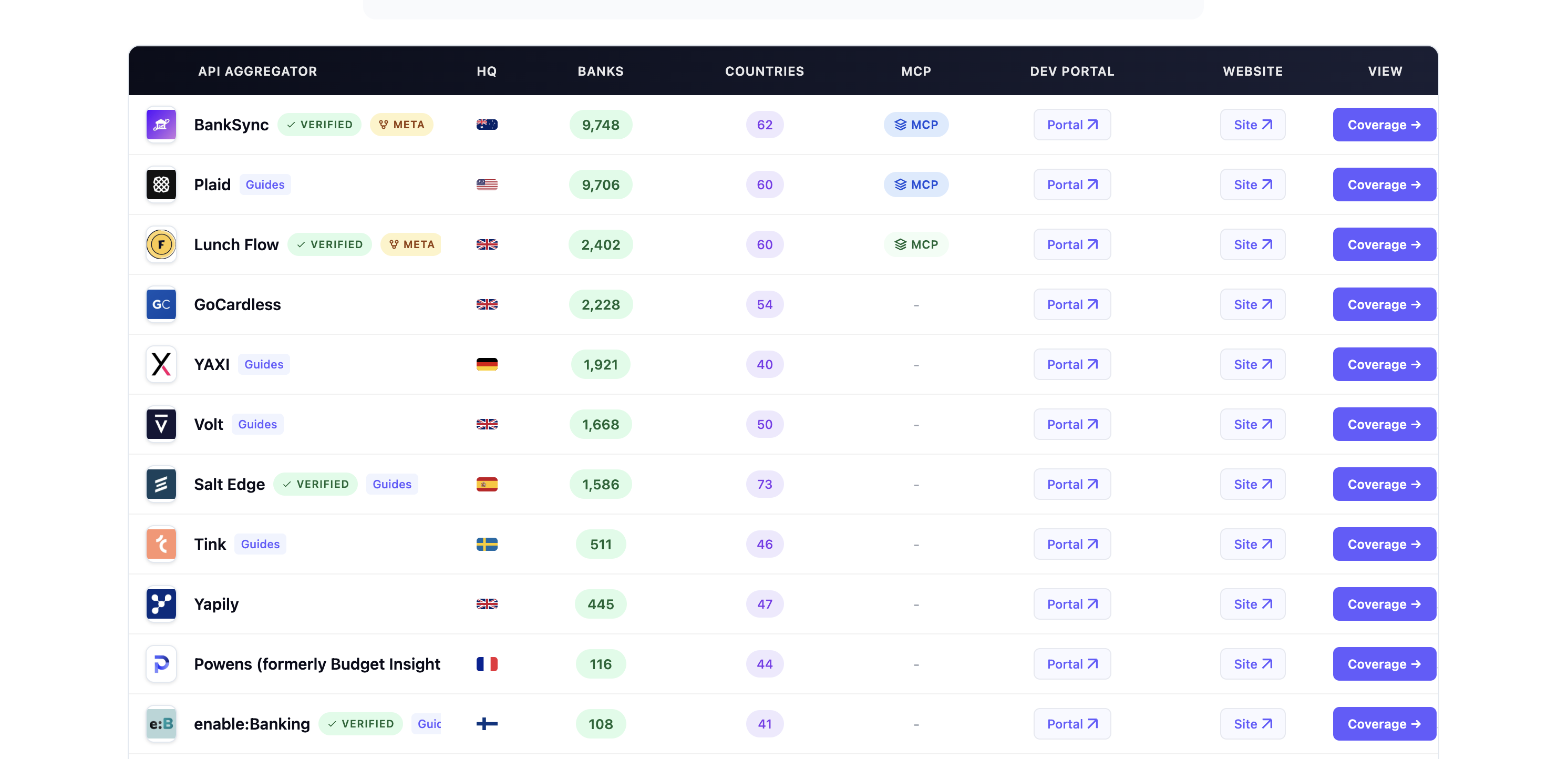

The Open Banking Tracker's Agentic Banking directory tracks which banks and financial platforms have published MCP servers, and the list is growing. Below are ten use cases with live or announced deployments behind them.

1. Read-only bank account queries

This is where almost every bank starts. A read-only MCP integration is low-risk, fast to build if you already have open banking APIs, and immediately useful for any AI assistant a business client is running.

Grasshopper Bank in New York was among the first U.S. banks to go live, built by their digital banking provider Narmi. Business clients can query account balances and categorize vendor spending directly through Claude. No export-then-reimport workflow. The data is in the conversation.

Slash, a U.S. business banking platform used by 5,000+ businesses, takes the same starting point further. Its hosted MCP server at mcp.slash.com exposes account balances, transaction history, and the full API schema to any compatible agent: Claude, GPT, or custom builds. Write operations like card creation and payments are available too, but sit behind human-in-the-loop approval and RSA-encrypted card data, so the agent can prepare and queue actions without executing them autonomously. That layered model, read freely and write with approval, is one of the cleaner permission architectures in production today.

2. ACH return processing

ACH returns follow a fixed rule set: return reason codes and timing windows, with clear resubmission criteria. There's no judgment call required for the majority of items. An agent can resolve straightforward returns and flag exceptions for human review in minutes, rather than queuing them for a back-office team to process end of day.

PCBB identified this in January 2026 as one of the highest-confidence near-term use cases for community financial institutions, precisely because the rule set is well-defined and the error modes are predictable.

3. Autonomous payment execution

Meow Technologies launched what it describes as the first full agentic banking platform in April 2026. The product lets AI agents open business accounts, issue cards, send payments, and manage invoicing via natural language. The architecture uses a permissioned MCP setup with transfer limits and role-based controls enforced at the API layer, not left to the agent to reason about. Meow has over $1 billion in assets on platform.

The constraint model matters. Agentic payment execution only works operationally if the bank defines the guardrails before the agent touches anything.

4. Proactive financial coaching

Personetics released an MCP server in late 2025 that exposes its financial behavior analysis and predictive analytics to bank-deployed AI agents. A practical output: an agent can identify that a business client's receivables cycle lengthened from 28 days to 45 days and surface that in whatever interface they're already using, rather than in a dashboard they have to log into.

Personetics cites research showing 84% of consumers would switch banks for access to that kind of contextual financial advice. Whether that figure holds under pressure is debatable, but the direction is clear.

5. On-chain stablecoin payments

Coinbase launched a Payments MCP server in September 2025 that lets AI agents conduct autonomous on-chain transactions using stablecoins. It builds on the x402 protocol, which uses HTTP's "402 Payment Required" status code to enable stablecoin payments directly over HTTP. Agents can pay for APIs, services, and paywalled content without subscriptions or manual checkout. Install path: npx @coinbase/payments-mcp.

This differs from most banking MCP work, which focuses on data access. Coinbase's implementation is about execution: the agent actually moves money.

6. FX rate comparison and execution

An agent with access to a customer's transaction data and real-time FX feeds can compare rates across providers and execute a transfer on the best available rail without the customer touching a screen. The infrastructure already exists. What's new is the agent layer tying data access, comparison logic, and payment initiation into a single workflow.

The open banking APIs that banks were required to build for regulators turn out to be exactly what agents need to do this. The pipes were built for compliance. Agentic banking is the first commercial use case that benefits from them at scale.

7. Loan underwriting and credit decisioning

Underwriting involves multi-stage probabilistic judgment across credit history, transaction data, and qualitative factors. IDC's 2026 banking predictions describe a model where one agent runs credit checks against defined risk criteria, a second estimates maximum unsecured exposure, and a supervisory agent evaluates and approves the combined output. The human underwriter reviews the recommendation rather than rebuilding it from scratch. Who is actually doing this varies by institution type.

AI-native lenders are the clearest production examples. Pagaya's Q2 2025 shareholder letter states that 100% of loans on their platform are underwritten without manual intervention, using 180+ data points including alternative credit signals. Upstart runs the same model across 100+ bank and credit union partners via API. These companies were built around automated decisioning from day one, which makes their production claims credible in a way that bank pilot announcements are not.

Large banks are mostly at the AI-assisted stage, not AI-driven. HSBC uses generative AI to draft credit analysis memos from analyst-supplied data. Wells Fargo ran a multi-agent system to re-underwrite 15 years of archived loan documents — autonomous retrieval, extraction, and cross-checking — but that was a historical compliance project, not live origination. A lot of what gets described as "bank AI underwriting" is Upstart or Zest AI running under a bank's brand.

McKinsey's December 2025 analysis found that most banks have not yet delivered efficiency gains at scale from AI. The IDC multi-agent supervisor model is a real design pattern, but public case studies of banks running it for live originations stay thin for two reasons: regulatory explainability requirements make full automation legally complicated, and banks have little incentive to advertise it. As fintech lenders prove the model at scale, the pressure on banks to follow will grow.

8. KYC and compliance automation

KYC checks involve pulling data from multiple sources, cross-referencing against watchlists, and assembling documentation for a compliance officer to review. The orchestration work fits multi-agent architecture: one agent queries data sources, another runs cross-reference checks, a supervisory agent flags discrepancies and assembles the file.

BNY Mellon's Eliza platform lets employees design AI agents with defined task scopes. Accenture's 2026 banking trends report recommends building an "agent identity framework" with authentication and permission controls across operations, which is the governance infrastructure KYC automation requires before it can run at any scale.

9. Cash flow monitoring and early warning

Mastercard announced Virtual C-Suite in March 2026, an agentic product that plugs into accounting systems and banking applications to give small businesses CFO-level financial analysis. The Virtual CFO module monitors cash flow and answers natural language questions like "What's driving this week's cash swing?"

The more valuable application is proactive. An agent with read access to a business client's accounts can spot a 30% drop in payroll deposits month-over-month and flag a potential cash flow problem before the client calls the bank. That's continuous monitoring with human-readable output, not analysis on demand.

10. Agentic commerce and lending discovery

This is the use case most banks haven't internalized yet. Salesforce's 2025 holiday shopping report found that AI agents influenced $262 billion in U.S. sales that season. The agent choosing which financing option to show at checkout does so based on which providers are accessible via API or MCP, not on which bank has the best website.

As Yaacov Martin, CEO of Jifiti, wrote in March 2026: banks not integrated via MCPs are progressively invisible to consumers who shop through AI-assisted channels. The discovery problem is already here. Banks solving it are treating their MCP server as a distribution channel, not just an internal automation tool.

The Agentic Banking directory tracks which financial institutions have official MCP servers live. If your bank has published one and isn't listed, submit it here.